Business insurance protects companies from financial losses through various policies like general liability, property, and workers' compensation.

Every business faces unique risks, and having the right insurance coverage is a critical component of a sound risk management strategy. It’s not just about fulfilling legal requirements; it’s about ensuring the long-term resilience and financial stability of your enterprise. This guide outlines the essential types of business insurance coverage to consider.

Thinking a license bond is about your work quality

Most contractors believe the Arizona Contractor License Bond guarantees their project performance. It doesn't. This bond is a financial guarantee to the state that you will follow licensing laws, pay owed taxes, and cover certain public liabilities from your business operations. The part most applicants underestimate is the personal credit check. Underwriters review your credit to assess the risk you'll default on the bond's financial obligation, not your skill as a contractor. A low score doesn't automatically disqualify you, but it directly impacts your premium rate and the speed of approval.

- The bond protects the public and state, not your client's project outcome.

- Your personal credit score is the primary factor determining your bond premium.

- You are personally liable for any claims paid by the surety on your bond.

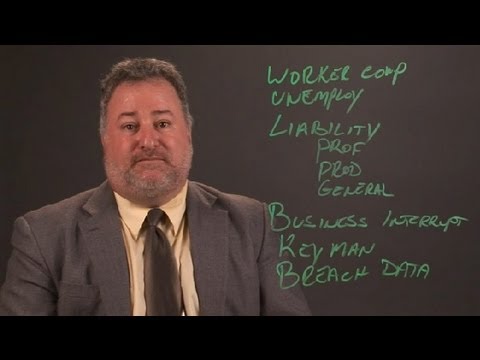

General Liability Insurance

This is foundational coverage for most businesses. It protects against claims of bodily injury, property damage, and personal injury (like slander) that occur due to your business operations. For instance, if a client slips and falls in your office, general liability insurance can help cover associated medical expenses and legal fees.

Professional Liability Insurance

Also known as Errors and Omissions (E&O) insurance, this is crucial for service-based businesses. It provides protection if a client alleges negligence, mistakes, or failure to deliver a service as promised. This coverage can help with legal defense costs and potential settlements.

Commercial Property Insurance

This insurance covers your business’s physical assets from covered perils like fire, theft, or storm damage. It applies to the building if you own it, as well as to equipment, inventory, furniture, and other essential business property located at the premises.

Business Interruption Insurance

Often added to a property insurance policy, this coverage helps replace lost income and cover operating expenses if your business is temporarily unable to operate due to a covered physical loss, such as fire or major weather damage. It is a vital safeguard for maintaining cash flow during recovery periods.

Workers’ Compensation Insurance

In most states, this insurance is legally required if you have employees. It provides benefits to employees who suffer work-related injuries or illnesses, covering medical costs and a portion of lost wages. In return, it typically protects the employer from lawsuits related to those incidents. For detailed information on state-specific requirements, you can refer to the U.S. Department of Labor’s Office of Workers’ Compensation Programs.

Choosing the Right Coverage

Selecting the appropriate insurance portfolio requires a careful assessment of your specific business risks. The optimal coverage mix depends heavily on your industry, location, number of employees, and the nature of your assets and operations.

To effectively evaluate your needs, consider the following key factors:

- Industry & Services: High-risk fields like construction or healthcare have vastly different liability exposures than a consulting firm.

- Business Assets: The value of your physical property, inventory, and specialized equipment directly influences necessary coverage levels.

- Number of Employees: This determines requirements for workers’ compensation and can affect liability premiums.

- Client Contracts: Many agreements require you to carry specific types and amounts of insurance.

Consulting with a licensed commercial insurance agent or broker is highly recommended. They can conduct a thorough risk assessment and help you tailor a policy that provides comprehensive protection without unnecessary overlap or costly gaps.