If you need a surety bond for your business, one of your first questions is likely, “How much will it cost?” The answer isn’t a single number, as bond premiums are calculated as a percentage of the total bond amount. This percentage, known as the premium rate, is determined by the surety company based on an assessment of risk.

What Factors Influence Surety Bond Costs?

Several key factors directly impact the premium rate you will be offered. Understanding these can help you prepare your application and potentially secure a more favorable rate.

- Personal Credit Score: For many commercial bonds, especially those not mandated by law, your personal credit history is a primary factor. Applicants with strong credit typically receive the standard market rate, while those with lower scores may face higher premiums due to the perceived increase in risk.

- Financial Statements: The surety will examine your company’s financial health, including balance sheets and income statements, to gauge stability and the ability to fulfill obligations.

- Industry Experience: Your track record and years in business demonstrate reliability and can positively influence the underwriter’s decision.

- Bond Type and Amount: The required bond amount set by the obligee (often a government agency) is the base for the premium calculation. Higher-risk bond types naturally command higher premium rates.

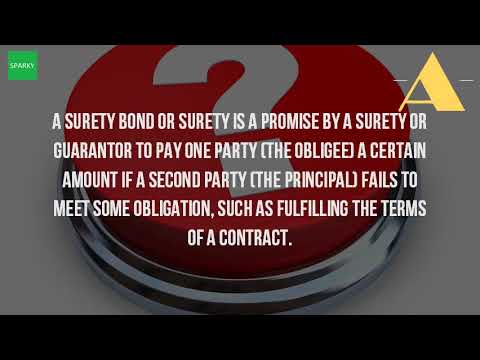

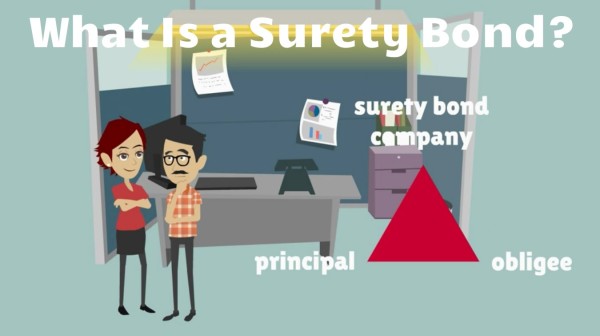

It’s a common misconception that surety bonds function like traditional insurance. While an insurance policy protects the policyholder against loss, a surety bond is a three-party agreement that guarantees the obligee (the project owner or government entity) that the principal (you or your business) will perform according to the terms of a contract or law. The surety company provides a financial guarantee of this performance.

Typical Surety Bond Cost Ranges

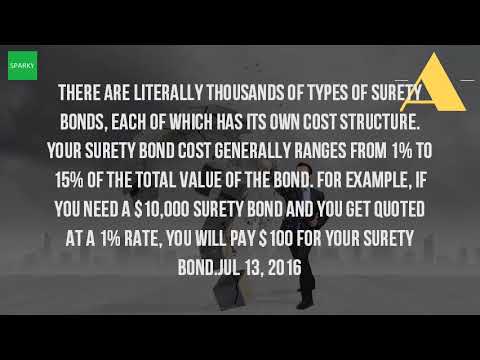

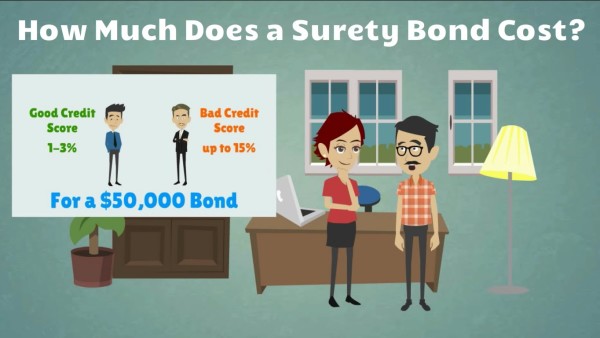

Premiums can vary widely, but most standard commercial surety bonds cost between 1% and 5% of the total bond amount for qualified applicants. For example, a $50,000 bond with a 2% premium rate would cost $1,000. High-risk applicants or specific bond types may see rates from 5% to 15% or more. It is crucial to get a personalized quote from a reputable surety bond provider or agency for an accurate price.

To navigate this process effectively, consider working with an experienced surety bond agency. These specialists act as intermediaries between your business and the surety markets. A knowledgeable agent can advocate on your behalf, help you present the strongest possible application, and shop your submission to multiple surety companies to find you the most competitive rate available.

For official information on bonding requirements for federal contracts, you can refer to the U.S. Small Business Administration website.