Bonds are debt securities where investors lend money to an issuer, such as a corporation or government, in exchange for regular interest payments and the return of the principal at maturity.

In this episode, we break down the fundamentals of bonds, a cornerstone of the fixed-income market. We’ll explain how they function as debt instruments and why they are a critical component of both corporate finance and diversified investment portfolios.

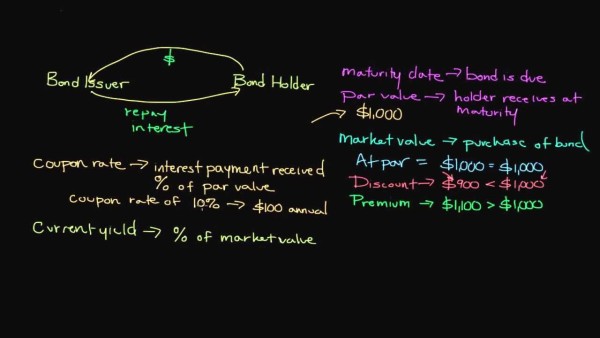

When you purchase a bond, you are essentially lending money to the issuer, which could be a corporation, a municipality, or a national government. In return for this loan, the issuer promises to pay you periodic interest payments, known as coupons, and to return the principal amount, or face value, on a specified maturity date. This contractual obligation makes bonds a more predictable investment compared to equities.

Understanding the relationship between bond prices and interest rates is crucial for any investor. When prevailing market interest rates rise, the fixed coupon payments of existing bonds become less attractive, causing their market prices to fall. Conversely, when market rates fall, existing bonds with higher fixed coupons become more valuable, and their prices tend to increase. This inverse relationship is a fundamental principle of bond investing.

Several key factors influence a bond’s risk and return profile:

- Credit Risk: The financial health of the issuer and its ability to make timely interest and principal payments. This is often reflected in credit ratings from agencies like Moody’s or Standard & Poor’s.

- Interest Rate Risk: The risk that rising market interest rates will cause the bond’s market value to decline, as explained above.

- Inflation Risk: The danger that inflation will erode the purchasing power of the bond’s future fixed interest payments and principal repayment.

- Term to Maturity: Generally, bonds with longer maturity dates are more sensitive to interest rate changes and may offer higher yields to compensate for this increased risk.

Bonds are not just simple loans; they are tradable securities with valuations that fluctuate daily in the secondary market. This liquidity allows investors to buy and sell bonds before they mature, providing flexibility that a standard bank loan does not offer. The U.S. Securities and Exchange Commission provides educational resources for investors looking to understand these public securities markets in greater depth.

For a deeper dive into specific bond types, such as municipal bonds which often offer tax-exempt income, you can refer to resources like the Investor.gov guide on bonds. We’ll explore different categories, including Treasuries, corporates, and municipals, in future episodes to help you build a robust fixed-income strategy.

Assuming your bond cost is just a simple percentage

The most costly mistake is thinking your Oregon contractor license bond premium is a fixed rate like 1% or 2% of the bond amount. In practice, your final cost is determined by an underwriter reviewing your personal credit score, financial statements, and business history. Applicants with lower credit often pay 3-5% or more. What slows this down is not having your financials ready. The part most applicants underestimate is how much a strong credit profile can reduce your annual premium.

- Your personal credit score is the primary factor in your final rate.

- Have 2 years of business and personal financial statements prepared for review.

- A higher bond amount doesn't mean a proportionally higher cost; underwriting is key.