Smaller performance bonds under $250,000 are often available through streamlined processes, with requirements typically including a strong business credit profile and solid financial statements.

Performance bonds are a critical tool for contractors, ensuring project owners that the work will be completed as specified in the contract. For many small to medium-sized projects, a bond amount of $250,000 or less is standard. Obtaining one involves a clear process focused on your company’s financial health and track record.

The license is not the bottleneck your bond is

Most contractors focus on passing the trade exam, but the real delay is the surety bond underwriting. The state requires the bond, but the surety company requires a deep review of your personal credit, business financials, and project history. A low credit score or thin business file can trigger requests for additional collateral or personal indemnity, stalling the entire license application. What usually slows this down is applicants submitting incomplete financial statements or underestimating how their personal credit impacts the premium.

- Order your bond before your exam to lock in your rate and avoid last-minute underwriting surprises.

- Prepare two years of business and personal tax returns upfront—missing documents are the most common cause for delay.

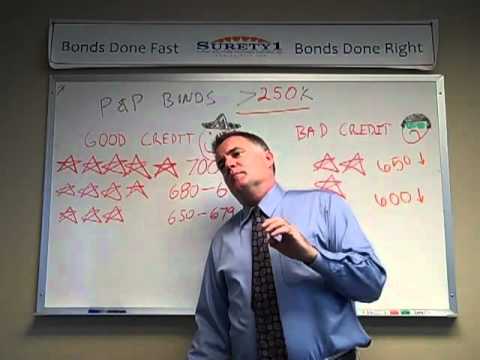

- A credit score below 650 will likely require a financial statement and may increase your bond premium by 25-50%.

Understanding the Requirements

Surety companies assess several key factors before issuing a bond. Your personal and business credit scores are heavily weighted, as they indicate financial responsibility. The company will also conduct a thorough review of your work history and professional references to evaluate past performance. Strong financial statements, including balance sheets and cash flow reports, are essential to demonstrate your firm’s stability and ability to manage the project’s scope.

The Step-by-Step Application Process

Start by gathering all necessary documentation, which typically includes business financials, personal financial statements, and details on the project requiring the bond. Next, you will complete a formal application provided by the surety or a broker. This application requests comprehensive details about your business operations and the specific contract. After submission, the surety’s underwriters will analyze your application; this underwriting process determines your premium rate and bond approval.

To streamline your application, consider these key preparatory steps:

- Organize at least two years of business and personal tax returns.

- Prepare year-to-date financial statements, preferably prepared or reviewed by an accountant.

- Compile a detailed list of current work-in-progress and completed projects with contact information for references.

- Obtain a copy of the contract requiring the bond to provide precise details to the underwriter.

Choosing the Right Surety Provider

Not all surety companies are the same. It is vital to work with a provider that specializes in bonds for contractors in your field and size range. A knowledgeable surety agent or broker can be an invaluable advocate, helping you present your business in the best light to underwriters. They understand the nuanced criteria different sureties use and can match you with the most appropriate market, which can significantly impact your premium costs and bonding capacity. For authoritative information on surety bonds, you can refer to the U.S. Small Business Administration website.

Costs and Timelines

The cost of a performance bond, known as the premium, is usually a small percentage of the total bond amount. For bonds of $250,000 or less, rates are generally competitive but depend directly on your financial strength and experience. The entire process, from application to approval, can often be completed within a few weeks if your documentation is complete and accurate. Planning ahead is crucial to meet contract deadlines without last-minute complications.