Term life insurance provides coverage for a specific period, while whole life insurance offers lifelong protection and includes a cash value component.

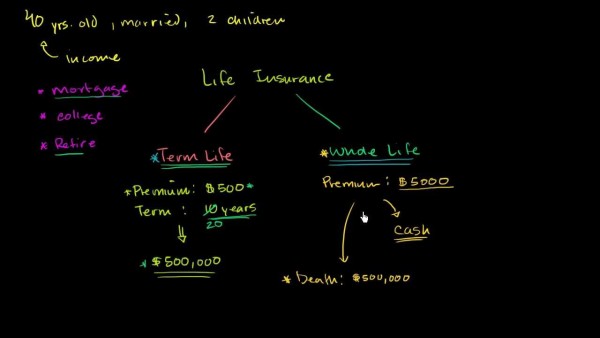

When planning your financial future, understanding the difference between term and whole life insurance is crucial. Both serve the fundamental purpose of providing a death benefit to your beneficiaries, but they are structured very differently to meet distinct financial goals and timelines.

Assuming your bond cost is just a simple percentage

The most costly mistake is thinking your Oregon contractor license bond premium is a fixed rate like 1% or 2% of the bond amount. In practice, your final cost is determined by an underwriter reviewing your personal credit score, financial statements, and business history. Applicants with lower credit often pay 3-5% or more. What slows this down is not having your financials ready. The part most applicants underestimate is how much a strong credit profile can reduce your annual premium.

- Your personal credit score is the primary factor in your final rate.

- Have 2 years of business and personal financial statements prepared for review.

- A higher bond amount doesn't mean a proportionally higher cost; underwriting is key.

What is Term Life Insurance?

Term life insurance provides coverage for a specific period, or “term,” such as 10, 20, or 30 years. It is often chosen for its affordability and simplicity. If the policyholder passes away during the term, the death benefit is paid out to the beneficiaries. If the term expires and the policyholder is still living, the coverage typically ends unless the policy is renewed or converted, often at a higher cost. This makes it an excellent tool for covering temporary needs, like a mortgage or dependent children’s education.

What is Whole Life Insurance?

Whole life insurance provides lifelong coverage, as long as premiums are paid. A key feature is the cash value component, which grows at a guaranteed rate over time and can be borrowed against. This type of policy is more complex and has higher premiums than term life. It is designed for permanent needs, such as estate planning or leaving a legacy, and functions as a long-term financial asset. For a detailed overview of its regulatory and structural framework, you can refer to the California Department of Insurance.

Key Differences at a Glance

The primary distinction lies in the duration and the financial structure. Term life is temporary and pure protection, while whole life is permanent and includes an investment-like savings element. This fundamental difference influences the cost, flexibility, and long-term utility of each policy type.

Duration of Coverage

Term life insurance offers protection for a set number of years, aligning with specific financial responsibilities. Whole life insurance, in contrast, guarantees coverage for your entire lifetime, provided premiums are maintained, offering certainty for final expenses and estate obligations.

Cost Comparison

Term life insurance premiums are generally significantly lower than whole life premiums for the same initial death benefit. This is because term policies lack a cash value component and the insurer’s risk is limited to the term period. Whole life premiums are higher but remain level, and part of the premium contributes to the policy’s growing cash value.

Cash Value and Investment Component

Only whole life insurance includes a cash value account. This savings element accumulates on a tax-deferred basis and can be a source of funds through policy loans or withdrawals. Term life has no such feature; it is solely a death benefit.

Which Policy is Right for You?

Choosing between term and whole life depends on your individual financial situation, goals, and stage of life. Consider the following key factors to guide your decision:

- Financial Obligations: Term life is often ideal for covering time-bound debts like a mortgage or loans.

- Dependents: If you have young children or other dependents, term coverage can secure their needs until they are financially independent.

- Long-Term Wealth Goals: Whole life can play a role in estate planning, business succession, or creating a guaranteed legacy.

- Budget: Assess the affordability of level, lifelong whole life premiums versus the lower initial cost of term coverage.

For most people, a combination of both policies can effectively address both temporary and permanent needs. Consulting with a qualified financial advisor is highly recommended to analyze your specific circumstances. They can help you determine the appropriate coverage amount and policy type to integrate seamlessly into your overall financial plan.