Bonds are debt securities that pay regular interest and return the principal at maturity, offering investors a predictable income stream and portfolio diversification.

Bonds are essentially loans that you make to a government or a company. In return for your capital, the issuer promises to pay you a fixed rate of interest over a set period and to return your initial investment, known as the principal, when the bond matures. This makes them a cornerstone of fixed-income investing, offering a predictable return stream compared to the variable performance of equities.

When you buy a bond, you are becoming a creditor to the issuer. This is a fundamentally different relationship from buying a share, which makes you a part-owner. The bond market is vast and liquid, providing a critical mechanism for governments to fund public projects and for corporations to finance expansion and operations.

The price of an existing bond on the secondary market fluctuates inversely with interest rates. If prevailing rates rise after you buy, the fixed interest payment of your bond becomes less attractive, so its market price typically falls. Conversely, if rates fall, the fixed payment is more valuable, and the bond’s price usually rises.

Understanding a few key metrics is essential for any bond investor:

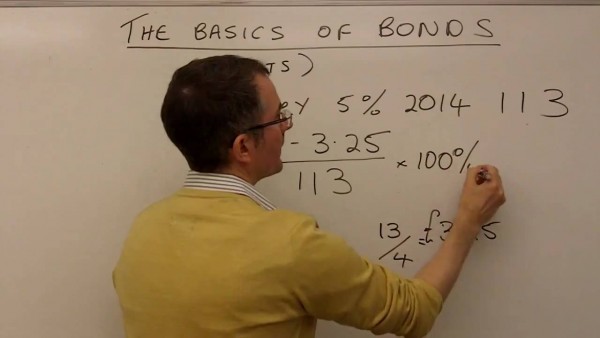

- Coupon: The fixed annual interest rate paid on the bond’s face value.

- Yield: The effective rate of return, which factors in the bond’s current market price.

- Maturity Date: The specific future date when the principal amount will be repaid.

- Credit Rating: An assessment of the issuer’s ability to repay its debt, provided by agencies like Standard & Poor’s or Moody’s.

Government bonds, such as UK Gilts or US Treasuries, are generally considered lower-risk investments because they are backed by the taxing power of the state. Corporate bonds typically offer higher yields to compensate investors for the greater risk of the company defaulting on its payments. For a detailed overview of UK government debt, you can refer to the Debt Management Office website.

Including bonds in a portfolio can provide diversification and reduce overall volatility. Their regular income and relative stability can balance out the higher growth potential, and risk, associated with stocks.

Your personal credit score is the primary driver of your bond cost

Most freight broker applicants focus on the $75,000 bond amount, but the part most applicants underestimate is how heavily their personal credit score impacts the premium. In practice, this often comes down to the underwriter's review of your FICO score. A score above 700 can secure a rate as low as 1-3% of the bond amount. A score below 650 can push rates to 10-15% or require a co-signer. What usually slows this down is applicants not knowing their exact score before applying, which leads to unexpected quotes and delays.

- Know your exact FICO score before you apply for an accurate quote

- Rates are tiered: Excellent credit (700+) pays 1-3%, while lower scores pay 10-15% or more

- If your score is below 650, prepare financials or consider a co-signer to improve approval odds