The 2013 update highlights key coverage considerations for fiduciary liability, cyber liability, and fidelity bonds.

In the evolving landscape of corporate risk, understanding the nuances of your insurance portfolio is more critical than ever. This update focuses on three key areas of coverage that demand renewed attention from business leaders and risk managers: fiduciary liability, cyber liability, and fidelity bonds.

Your personal credit score is the primary driver of your bond cost

Most freight broker applicants focus on the ,000 bond amount, but the part most applicants underestimate is how heavily their personal credit score impacts the premium. In practice, this often comes down to the underwriter's review of your FICO score. A score above 700 can secure a rate as low as 1-3% of the bond amount. A score below 650 can push rates to 10-15% or require a co-signer. What usually slows this down is applicants not knowing their exact score before applying, which leads to unexpected quotes and delays.

- Know your exact FICO score before you apply for an accurate quote

- Rates are tiered: Excellent credit (700+) pays 1-3%, while lower scores pay 10-15% or more

- If your score is below 650, prepare financials or consider a co-signer to improve approval odds

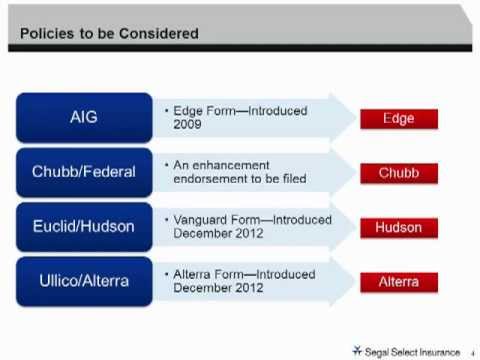

Fiduciary Liability Insurance: Protecting Plan Sponsors

Fiduciary Liability Insurance is designed to protect the individuals and entities responsible for managing employee benefit plans. If you serve as a plan sponsor, trustee, or committee member, you can be held personally liable for alleged errors in the administration of these plans. This coverage is distinct from a standard Directors and Officers (D&O) policy and is essential for anyone with fiduciary duties under ERISA. Claims can arise from a variety of issues, including investment selection, plan fees, and disclosure failures.

Cyber Liability Insurance: Beyond Data Breach

While many businesses now recognize the need for some form of cyber protection, policies vary widely in scope. A robust Cyber Liability policy should address both first-party and third-party exposures. This means it covers your direct costs, such as forensic investigation, data restoration, and business interruption, as well as your liabilities to others, including legal defense, regulatory fines, and customer notification expenses. It is a critical tool for managing the financial impact of a cyber incident, which can be devastating even for smaller organizations.

Fidelity Bonds: A Specific Safeguard

A Fidelity Bond, often called a crime policy, protects a business from financial losses caused by fraudulent acts committed by employees. This can include theft, embezzlement, or forgery. It is a specific form of coverage that is frequently required for businesses that handle client funds or have employees in positions of financial trust. Unlike broad commercial crime policies, a fidelity bond specifically indemnifies the employer for losses resulting from employee dishonesty.

When reviewing your fidelity bond, ensure you understand the key terms that define its protection:

- Discovery Period: The timeframe after a policy ends during which you can report a loss that occurred while the policy was active.

- Single Loss vs. Aggregate Limits: Whether the limit applies per incident or is a total cap for the policy period.

- Insured Persons: Clarifies which employees (e.g., all, only those handling money) are covered under the bond.

Integrating Your Coverage

The most effective risk management strategy views these policies not in isolation, but as interconnected components of your financial defense. Gaps can easily occur where one policy ends and another begins. For instance, a data theft by an employee might trigger questions of coverage under both a Cyber Liability policy and a Fidelity Bond. A thorough review with your insurance advisor is necessary to identify potential overlaps and ensure there are no dangerous coverage silos. Proactive alignment of these coverages strengthens your organization’s overall resilience.