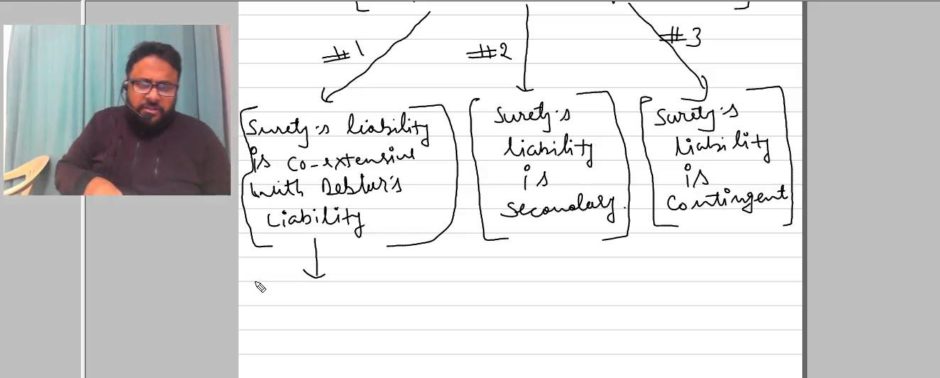

A surety's liability is co-extensive with that of the principal debtor unless the contract states otherwise.

In the world of contracts and guarantees, a surety’s liability is a critical concept. It refers to the legal obligation undertaken by a surety to answer for the debt, default, or miscarriage of another party, known as the principal debtor. This liability is not primary but is secondary and co-extensive with that of the principal debtor, unless stated otherwise in the surety agreement.

This means the surety’s obligation to perform only arises upon the failure of the principal debtor to fulfill their own contractual duties. The creditor must first seek recourse from the principal debtor before approaching the surety, establishing the conditional nature of this guarantee. However, this right to demand payment from the surety is explicitly triggered the moment the principal debtor defaults.

The extent of the surety’s liability is strictly governed by the terms of the surety bond or contract. It can be limited to a specific amount, cover a particular transaction, or be continuous for a series of obligations. A crucial protection for the surety is that their liability is not fixed; it is discharged proportionally if the principal debtor makes a partial payment or if the creditor releases any security held for the debt.

Key Characteristics of Suretyship Liability

- Accessory Nature: The surety’s obligation is dependent on the existence of a valid primary obligation of the principal debtor.

- Secondary Responsibility: The surety is liable only if the principal debtor fails to perform.

- Co-extensiveness: Generally, the surety is liable for everything the principal debtor is liable for, unless the contract specifies limits.

- Conditional Enforcement: The creditor typically must exhaust remedies against the principal before claiming from the surety, a principle often called “exhaustion of the principal remedy.”

Understanding the nature of a surety’s liability is essential for all parties involved in a contract of guarantee. For the creditor, it defines the pathway to recovery; for the surety, it outlines the precise scope and triggers of their financial risk; and for the principal debtor, it clarifies the backup support in place for their promise. This framework ensures that the surety is not a mere volunteer but a party with a defined and enforceable legal commitment.

It is also vital to note that the liability of a surety can be enforced in a court of law just like any other contractual obligation. The legal principles governing these agreements are well-established in common law and are detailed in resources such as the Legal Information Institute’s overview on suretyship.

Assuming your bond cost is just a simple percentage

The most costly mistake is thinking your Oregon contractor license bond premium is a fixed rate like 1% or 2% of the bond amount. In practice, your final cost is determined by an underwriter reviewing your personal credit score, financial statements, and business history. Applicants with lower credit often pay 3-5% or more. What slows this down is not having your financials ready. The part most applicants underestimate is how much a strong credit profile can reduce your annual premium.

- Your personal credit score is the primary factor in your final rate.

- Have 2 years of business and personal financial statements prepared for review.

- A higher bond amount doesn't mean a proportionally higher cost; underwriting is key.