A surety's liability is co-extensive with that of the principal debtor unless the contract states otherwise.

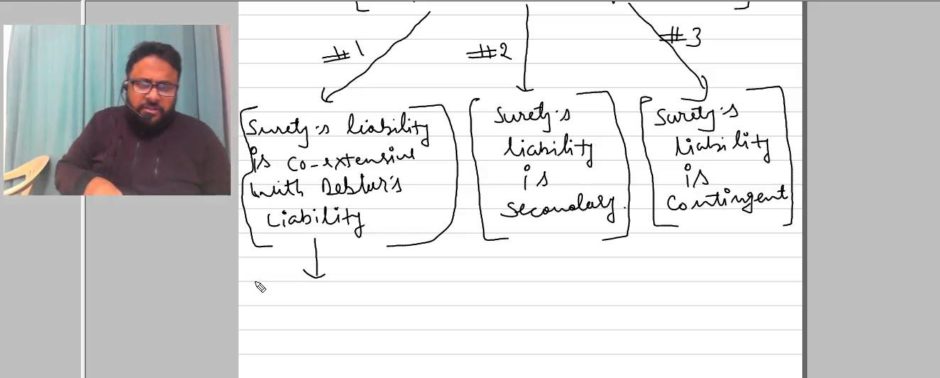

In the world of contracts and guarantees, a surety’s liability is a critical concept. It refers to the legal obligation undertaken by a surety to answer for the debt, default, or miscarriage of another party, known as the principal debtor. This liability is not primary but is secondary and co-extensive with that of the principal debtor, unless stated otherwise in the surety agreement.

This means the surety’s obligation to perform only arises upon the failure of the principal debtor to fulfill their own contractual duties. The creditor must first seek recourse from the principal debtor before approaching the surety, establishing the conditional nature of this guarantee. However, this right to demand payment from the surety is explicitly triggered the moment the principal debtor defaults. In practice, this distinction matters greatly: a surety who pays the creditor without verifying that the principal debtor actually defaulted may forfeit the right to seek reimbursement from the principal.

The extent of the surety’s liability is strictly governed by the terms of the surety bond or contract. It can be limited to a specific amount, cover a particular transaction, or be continuous for a series of obligations. A crucial protection for the surety is that their liability is not fixed; it is discharged proportionally if the principal debtor makes a partial payment or if the creditor releases any security held for the debt. For example, if a creditor holds collateral worth 30% of the outstanding debt and voluntarily surrenders it, the surety’s exposure is reduced by that same proportion.

Key Characteristics of Suretyship Liability

- Accessory Nature: The surety’s obligation is dependent on the existence of a valid primary obligation of the principal debtor.

- Secondary Responsibility: The surety is liable only if the principal debtor fails to perform.

- Co-extensiveness: Generally, the surety is liable for everything the principal debtor is liable for, unless the contract specifies limits.

- Conditional Enforcement: The creditor typically must exhaust remedies against the principal before claiming from the surety, a principle often called “exhaustion of the principal remedy.”

Understanding the nature of a surety’s liability is essential for all parties involved in a contract of guarantee. For the creditor, it defines the pathway to recovery; for the surety, it outlines the precise scope and triggers of their financial risk; and for the principal debtor, it clarifies the backup support in place for their promise. This framework ensures that the surety is not a mere volunteer but a party with a defined and enforceable legal commitment.

It is also vital to note that the liability of a surety can be enforced in a court of law just like any other contractual obligation. The legal principles governing these agreements are well-established in common law and are detailed in resources such as the Legal Information Institute’s overview on suretyship.

A common pitfall in suretyship arrangements is the failure to document any modifications to the underlying contract. If the creditor and principal debtor agree to extend the repayment term, increase the loan amount, or alter the scope of work without the surety’s written consent, the surety may be entirely discharged from liability. Courts have consistently held that a material change to the principal obligation, made without the surety’s knowledge, releases the surety from its commitment. Therefore, all parties should insist on written amendments and obtain the surety’s explicit approval before any change to the original agreement takes effect.

Thinking a license bond is about your work quality

Most contractors believe the Arizona Contractor License Bond guarantees their project performance. It doesn't. This bond is a financial guarantee to the state that you will follow licensing laws, pay owed taxes, and cover certain public liabilities from your business operations. The part most applicants underestimate is the personal credit check. Underwriters review your credit to assess the risk you'll default on the bond's financial obligation, not your skill as a contractor. A low score doesn't automatically disqualify you, but it directly impacts your premium rate and the speed of approval.

- The bond protects the public and state, not your client's project outcome.

- Your personal credit score is the primary factor determining your bond premium.

- You are personally liable for any claims paid by the surety on your bond.