Surety bond costs typically range from 1% to 15% of the bond amount, determined by factors like the applicant's credit score and the bond's risk level.

If you’re in the market for a surety bond, your first question is likely about cost. The price of a surety bond, known as the premium, is not a fixed number. It is determined by a combination of key factors that underwriters evaluate to assess risk. Understanding these variables is the first step to getting an accurate quote for your specific situation.

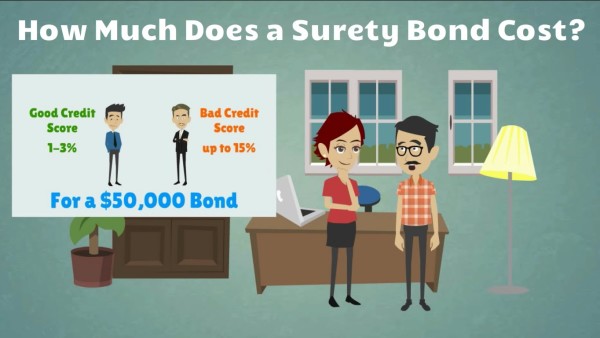

Your personal credit score is the primary driver of your bond cost

Most freight broker applicants focus on the ,000 bond amount, but the part most applicants underestimate is how heavily their personal credit score impacts the premium. In practice, this often comes down to the underwriter's review of your FICO score. A score above 700 can secure a rate as low as 1-3% of the bond amount. A score below 650 can push rates to 10-15% or require a co-signer. What usually slows this down is applicants not knowing their exact score before applying, which leads to unexpected quotes and delays.

- Know your exact FICO score before you apply for an accurate quote

- Rates are tiered: Excellent credit (700+) pays 1-3%, while lower scores pay 10-15% or more

- If your score is below 650, prepare financials or consider a co-signer to improve approval odds

What Factors Influence Surety Bond Costs?

Several core elements directly impact your bond premium. The single most important factor is the applicant’s personal credit score. Individuals with strong credit histories represent a lower risk to the surety company and will qualify for the lowest premium rates, typically between 1% and 3% of the bond amount. Conversely, applicants with lower credit scores may see premiums ranging from 3% to 10% or higher, as the perceived financial risk increases.

The bond amount itself, also called the penal sum, is the next major determinant. This is the maximum financial guarantee the bond provides. Since the premium is a percentage of this amount, a higher bond limit directly results in a higher premium cost. For example, a $50,000 bond at a 2% rate costs $1,000, while a $100,000 bond at the same rate costs $2,000.

Industry risk and bond type also play a significant role. Certain professions, like construction contractors or those handling client funds, are viewed as higher risk. A performance bond for a large project will be underwritten more rigorously—and often cost more—than a simple license bond for a low-risk business.

Finally, the required bond term influences the total price. Most bonds are issued for one-year terms and must be renewed annually, with premiums paid each term. Some bonds may be written for multiple years, which can affect the total cost calculation.

How to Get the Best Surety Bond Rate

To secure the most favorable rate, preparation is key. Start by obtaining a copy of your personal and business credit reports to understand your financial standing. Disclose all relevant information accurately on your application, as transparency builds trust with underwriters. It is also highly advisable to work with an experienced surety bond agency. A knowledgeable agent can advocate on your behalf, present your financials in the best light, and leverage their relationships with multiple surety companies to find you the most competitive offer.

When comparing quotes, look beyond just the premium percentage. Consider the surety company’s financial strength, its reputation for handling claims, and the agency’s level of customer service. The cheapest bond is not always the best value if the provider is difficult to work with or financially unstable.

Common Surety Bond Types and Typical Costs

While costs vary, here are general premium ranges for common bond types, assuming standard credit:

- License & Permit Bonds: Often required by government agencies for businesses like contractors, motor vehicle dealers, and notaries. Premiums are typically 1% to 3% of the bond amount.

- Court Bonds: These include fiduciary (e.g., estate executor) and appeal bonds. They are highly case-specific but generally range from 1% to 5%.

- Contract Bonds: Required for construction projects (bid, performance, and payment bonds). These are heavily underwritten and typically cost 1% to 3% of the contract value.

- Commercial Bonds: This broad category includes bonds like those for freight brokers or Medicare providers. Premiums can vary widely, from 1% to 10%, based on risk.

Next Steps for Your Surety Bond

Getting a surety bond doesn’t have to be a complex process. By understanding the cost factors and preparing your financial information, you can approach the market with confidence. The best course of action is to request quotes from a few reputable surety bond providers to compare rates and terms specific to your bonding requirement.