What is Liability Insurance?

Liability insurance is a type of coverage that protects your business if you are found legally responsible for injuries to others or damage to their property. It helps cover the costs of legal defense, settlements, and court-ordered judgments, which can be financially devastating for a small business to pay out-of-pocket.

Why Your Business Needs It

Accidents and lawsuits can happen to any business, no matter how careful you are. A customer could slip and fall in your store, a client could sue you for a professional mistake, or your product could cause unintended harm. Without liability insurance, your business assets, and even your personal assets, could be at risk to cover these costs. It is a fundamental layer of financial protection that safeguards your company’s future.

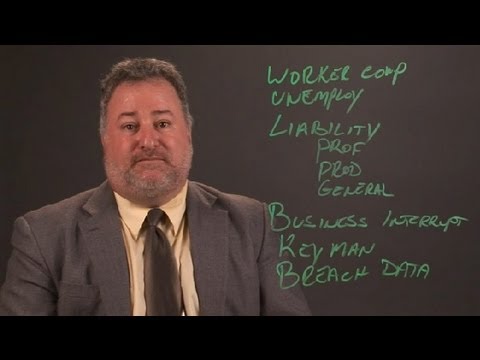

Types of Liability Coverage

There are several common types of liability insurance for small businesses:

- General Liability Insurance: This is the most common form, covering third-party bodily injury, property damage, and personal/advertising injury claims.

- Professional Liability Insurance: Also known as Errors and Omissions (E&O) insurance, it covers claims of negligence, mistakes, or failure to deliver a service as promised.

- Product Liability Insurance: Essential for businesses that manufacture or sell goods, this covers injuries or damages caused by a product you made or sold.

Many businesses start with a Business Owner’s Policy (BOP), which bundles general liability with property insurance at a discounted rate. This integrated approach is often recommended by the U.S. Small Business Administration as a cost-effective foundation for coverage.

How to Choose the Right Policy

Selecting the right liability insurance requires a careful assessment of your specific business risks. Consider the nature of your work, the number of employees you have, your business location, and the types of clients you serve. It is highly advisable to consult with a licensed insurance agent or broker who specializes in commercial policies. They can conduct a thorough risk analysis and help you compare quotes and coverage details from multiple carriers to find a policy that offers robust protection without unnecessary extras.

When evaluating policies, pay close attention to the coverage limits, deductibles, and any exclusions listed in the terms. A policy with a lower premium might have significant coverage gaps or sub-limits that could leave you exposed in the event of a major claim.

- Review Industry Requirements: Some professions or commercial leases legally require specific types and minimum amounts of liability coverage.

- Assess Client Contracts: Many client agreements, especially for contractors and consultants, stipulate mandatory insurance coverage and additional insured status.

- Plan for Growth: Consider how your policy can scale with your business, as taking on larger projects or hiring employees typically increases your liability exposure.

Next Steps

Getting liability insurance is a critical step in operating a responsible and resilient business. Start by gathering information about your operations and reaching out to insurance providers for quotes. Make sure you fully understand what each policy covers and what it excludes before making your final decision.