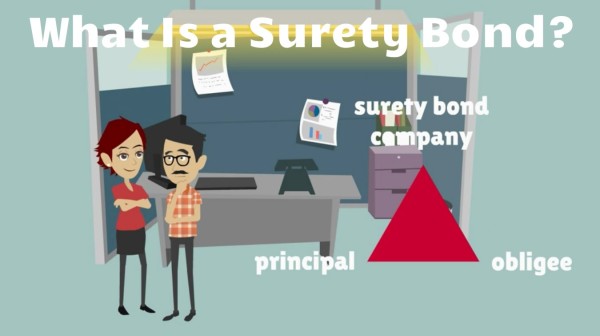

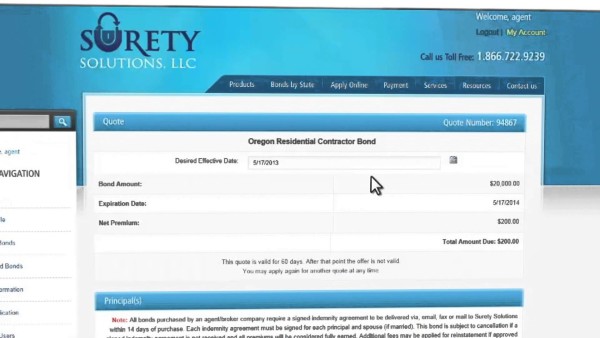

For many contractors, surety bonds are a necessary part of doing business. They are often required for public projects and large private contracts. A bond is a three-party agreement that guarantees project completion. It protects the project owner from financial loss if you fail to meet the contract terms.

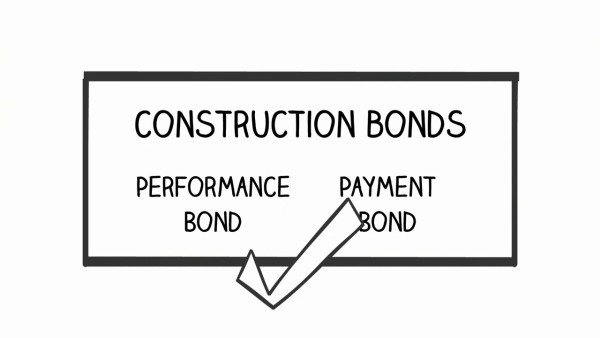

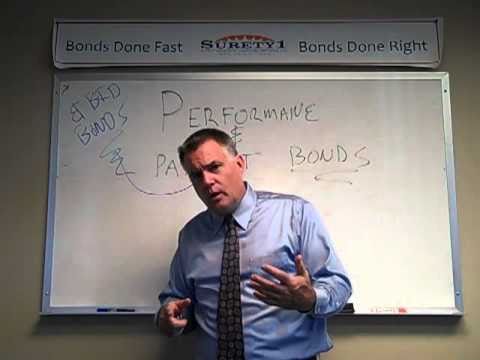

There are several common types of bonds you might encounter. A bid bond ensures your bid is submitted in good faith. A performance bond guarantees you will complete the project as specified in the contract. A payment bond assures that you will pay your subcontractors and suppliers. Knowing which type you need is crucial.

Maintaining bond eligibility requires strong financials. Sureties look at your company’s credit history, work experience, and financial stability. They want to see that you have the capacity to complete the job. A history of successful, profitable projects is your best asset.

To improve your chances of approval, organize your financial documents. This includes balance sheets, profit and loss statements, and cash flow projections. Be prepared to explain your business plan and the specifics of the project you’re bidding on. Transparency builds trust with the surety.

Before applying for a bond, it’s wise to review your company’s financial health. Address any outstanding debts or liens. Ensure your business licenses and registrations are current. A clean operational record demonstrates reliability to the surety company.

Building a relationship with a surety bond agent or broker can be highly beneficial. They can guide you through the process and help you present your business in the best light. A good agent will explain the underwriting criteria and help you find the right bond for your specific needs.

- Gather and organize two to three years of business and personal tax returns.

- Prepare detailed job cost histories for your recent major projects.

- Update your business plan to include current market positioning and future goals.

- Obtain a current business credit report to identify and address any discrepancies.

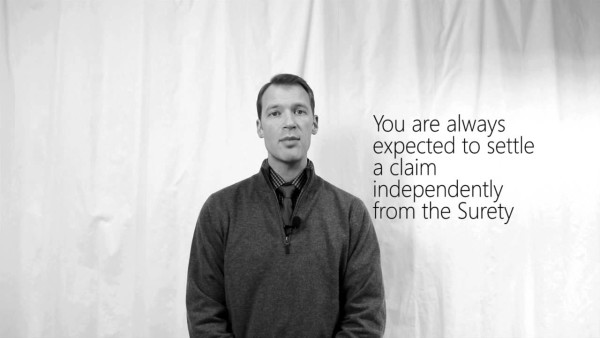

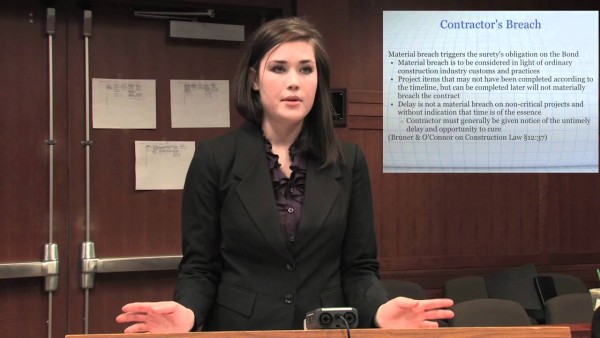

Remember, a surety bond is not insurance. It is a guarantee of your performance and financial responsibility. The surety company is taking a risk on your ability to fulfill the contract. If a claim is made against your bond, you are ultimately responsible for reimbursing the surety for any losses paid.

For more detailed information on the legal framework and public policy behind surety bonds, you can refer to the U.S. Small Business Administration website.