A Deeper Look At Bid Bond Examples

A lot of bond brokers just sell bonds, we produce them. Asking for a bid bond will certainly maintain service providers from submitting unimportant proposals, as a result of they could be bound to carry out the task, or a minimum of pay the bond costs.

Instance: Major Construction accepted start deal with the Precision Workplace Constructing on 1/1/09 but had not even damaged ground on 4/1/09. Accuracy Workplace takes into consideration Main to be in default as well as informs the guaranty company. The guaranty chooses to forfeit the charge as a substitute of getting worried in a protracted-time period building procedure and due to the fact that the contrary bids throughout the affordable bidding process on the task had actually been considerably greater than Main’s. The guaranty firm is worried that the agreement rate could likewise be inadequate to complete the task.

An Overview

As discussed above, the required proposal demand type requests for contract particulars such as the job worth failure, that includes earnings, materials, labor, subcontractors as well as overhead. Offering these particulars may be complicated and also tough when making an attempt to file in a paper system. That is where construction proposal software program can be found in; it can be utilized to estimate your agreement costs and also consider and also handle your organization’s crucial metrics Harnessing the ability of software program offers you with a much better opportunity at lucrative the initiatives you need.

Lots of subcontracts in the here and now day consist of a “pay when paid” provision, calling for fee to a sub when the proprietor pays the basic specialist for the below’s work being billed.

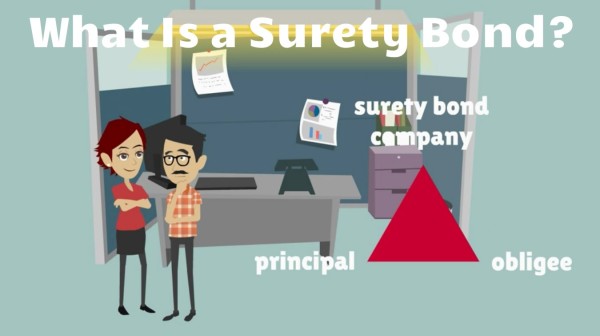

A type of guaranty bond made use of by capitalists in construction initiatives to safeguard versus a hostile celebration that causes disruptions, failing to finish the endeavor resulting from bankruptcy of the contractor( s), or the job’s failure to meet contract specifications.

- Bid bonds typically require the contractor to provide financial statements and project history to demonstrate capability.

- The bond amount is often a percentage of the bid price, commonly between 5% and 10% for federal projects.

- Claiming a bid bond usually involves proving the contractor failed to execute the contract after award.

What Is A Construction Surety Bond?

Arms, turbines, radio towers, tree removal, computer systems, softward, fire place alarms, attractive job, scaffolding, water towers, lighting, and resurfacing of present roads/paved areas. One other manner guaranty companies can keep within their authorised guaranty underwriting limit, and also unfold their danger, is to obtain coinsurance or reinsurance, during which they basically acquire an agreement from an additional guaranty firm to cowl part of their risk on the bond they’ve released. When a surety gets reinsurance for a part of its risk below a miller act bond, it must submit to the having officer a reinsurance negotiation for a Miller Act performance bond as well as a reinsurance negotiation for a Miller Act repayment bond. The expressions of both reinsurance agreements are specified within the laws.

Should the service provider be granted the quote, the bond exists to ensure that the agreement will be executed at the quote worth and also listed below the scenarios set forth in the quote. If the agreement isn’t performed in line with the proposal, a state in opposition to the bond can be made.

When Referring To Examples

Personal building tasks in addition utilize this twin bond procedure as a result of the different Fee bond reduces the submitting of labor and/or products liens in the direction of the owner’s home that might encumber the owner’s title. Whereas a lien for non-fee of labor as well as products settlements can’t be connected to public residential or commercial property, it’s thought-about excellent public coverage to assure such expense. This use avoids forcing products vendors so as to include extreme worth hundreds with the intention to address in any other situation unsecured dangers. For more information on bid bond requirements in federal contracting, see the Federal Acquisition Regulation Part 28.